AFRICA FINTECH OVERVIEW

PUBLIC MARKETS

The Imara African Opportunities Fund, investing in listed fintech and payment companies, is up 8.6% in February.

Despite a tough global backdrop, positive developments in Africa continued unabated. 4q25 results hitting the tape are extremely strong and large, long term investors are buying African businesses at substantial premia to listed valuations. Nedbank has made an offer to buy NCBA in Kenya at an implied price to book of 1.4x, a substantial premium to the region’s leader, Equity Bank, which trades at a 0.9x book on the Nairobi exchange.

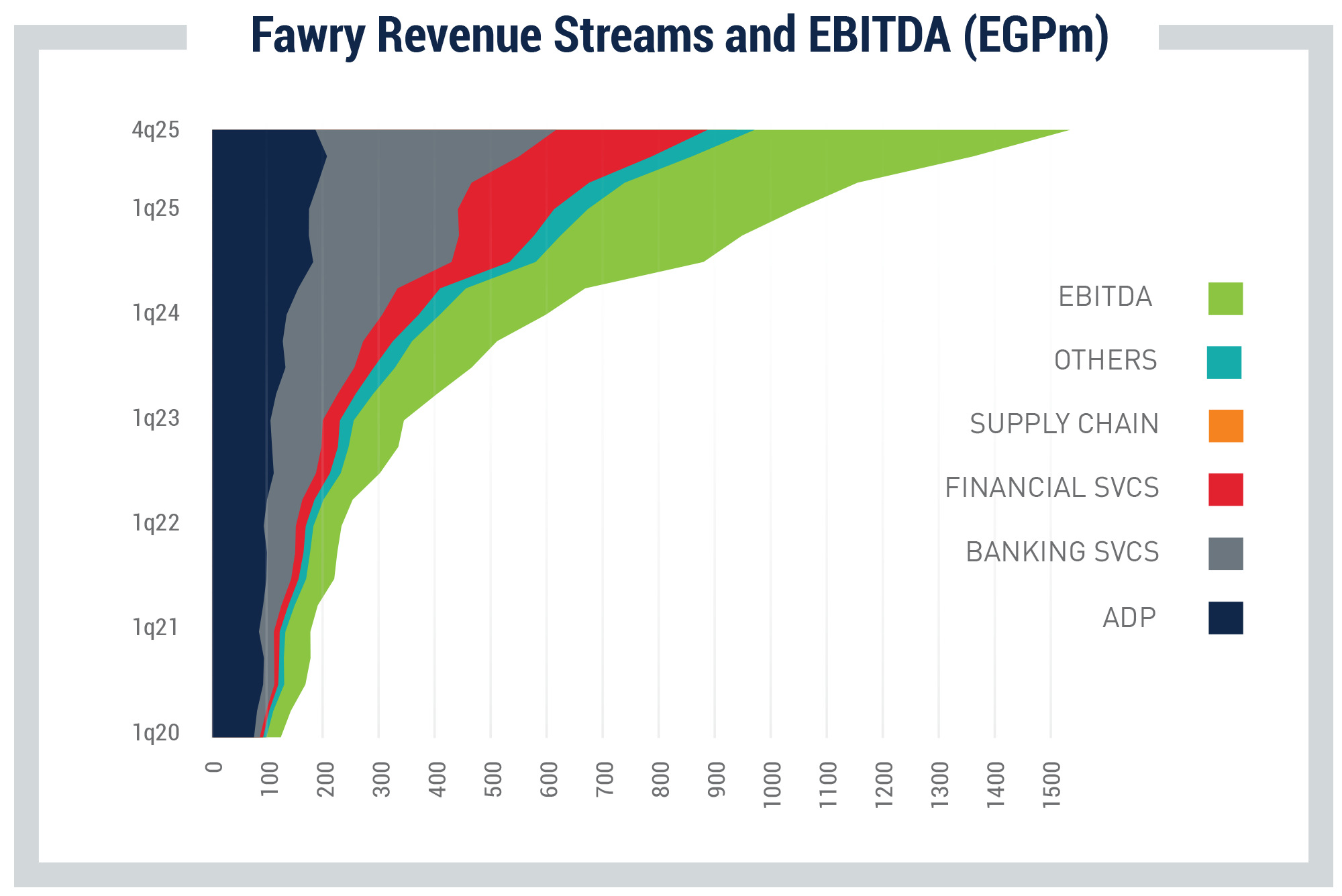

Time for results. Fawry - a great example of WIDTH and LENGTH of runway to visualize the GROWTH and PROFITABILITY prospects of our investments. To demonstrate the concept of long and wide runways, it would be hard to find a better example than Fawry, one of our key positions in the Egyptian fintech space. The chart below shows the evolution and contribution from 1q20 to 4q25 to revenues by the different streams, as well as the growth, in Green, of EBITDA. The Green line is critical, as we have long argued that these new revenues carry little incremental cost and therefore boost margins. Over the period, EBITDA has grown a fantastic 22-fold. Egypt's extremely low penetration of financial services will ensure that these growth rates will continue into the foreseeable future.

For the fourth quarter specifically, revenues grew 56%, EBITDA +74% and EPS a whopping 71%. From a valuation perspective, Fawry trades at a forward EV/EBITDA of 8.5x and an EV/Revs of 4.5x, with a PE of 13x. This is extremely cheap for a company growing this fast and with a RoE of 48%!

Next up, Equity Bank – reported 2025 EPS +55% and a DPS +36% and equating to a yield of 7.5%. The bank generates a return of 27% RoE, despite retaining two thirds of earnings. It trades on a forward price to book value of 0.9x, which is ridiculously low relative to financial performance and recent deal multiples.

MTN also reported strong numbers for 2025, with revenues coming in +23% and EBITDA +37%. EPS was up 67% with a RoE of 26%. Within that, Fintech revenue was up 23%. The Group now serves a whopping 307m subscribers, of which 70m mobile money customers. It trades on an attractive forward EV/EBITDA of 3.5x.

For more insights and developments, please our detailed country sections in the body of the report.

VENTURE CAPITAL AND PRIVATE EQUITY DEAL UPDATE

- Trove Finance, the Nigerian wealth-tech startup, has acquired UCML Securities (now rebranded Innova Securities), giving Trove its own SEC-licensed broker-dealer after years of relying on partners. This allows Trove to tighten control over trade execution and compliance as it eyes deeper product expansion.

- Lula raised $21 million from Dutch development bank FMO to expand its tech-driven lending platform, building on $35 million Series B and prior IFC support. The fintech’s platform delivers fast, flexible working capital to businesses often ignored by banks.

- Beltone Holding has finalised its $197.6 million acquisition of Baobab Group, giving the Cairo firm an instant footprint across seven African markets. Baobab’s €848.8 million loan book and 1.6 million customers now fold into Beltone’s push to become a tech-led MSME lender rather than a traditional brokerage. The deal also gives Baobab’s shareholders (including Apis Partners and Abler Nordic) a full exit.

- WafR, a Moroccan embedded-finance upstart, closed a $4 million seed round co-led by LoftyInc, Attijariwafa Ventures, and Al Mada. The startup powers 20,000 neighborhood retailers with mobile money services and is posting 29% monthly transaction growth. They’re aiming for 100,000 active merchants, and new products like micro-insurance and credit scoring for a market shifting quickly away from cash.

- Lupiya, a Zambian digital lender, has extended its Series A to $11.25 million, led by Alitheia IDF with support from INOKS Capital and DEG. The round’s been almost two years in the making and will fuel tech upgrades, new products, and expansion beyond Zambia.

ECONOMIC AND POLITICAL OVERVIEW

NIGERIA

The government has secured a USD 100m investment from the European Bank for Reconstruction and Development (EBRD) for Nigeria’s Project BRIDGE, the federal government’s fibre-optic expansion programme.

Nigeria has unveiled an ambitious plan to channel up to 5% of Nigeria’s GDP annually into industrial development financing, signalling a decisive pivot toward large-scale production, export competitiveness and job creation.

Nigeria’s average crude oil production in 2025 increased to 1.64 million barrels per day (mbpd), representing a 5.8% year-on-year rise from 1.55mbpd in the corresponding period of 2024.

The Nigerian Revenue Service (NRS) has said the country’s transition to mandatory electronic invoicing (e-invoicing) will be completed by January 2028 under a phased three-year implementation plan aimed at strengthening compliance and automating tax administration.

The Nigerian Revenue Service (NRS) generated N28.3 trillion in tax revenue in 2025, representing a 30% increase over the N21.7 trillion recorded in 2024.

Nigerian pension funds investments in infrastructure funds grew by 48.1% to N262bn in 10 months ended October 2025, driven by diversification strategy and efforts to bridge the nation’s massive infrastructure gap.

Macro releases included (January stats):

- Inflation decreased to 15.1% y/y (Dec: 15.2%).

- FX reserves increased to USD 50.5bn (Dec: USD 45.0bn).

- PMI was 49.7 (Dec: 53.5.2).

EGYPT

Egypt’s Remittance inflows rose 40.5% in 2025 to USD 41.5bn.

The Suez Canal Authority recorded a 22% y/y increase in revenues so far this year to USD 449mn. The number of passing vessels increased 6% to 1,315 vessels while carried tonnage rose 19% to 56mn tons.

The Egyptian economy recorded its highest growth rate in more than three years, expanding 5.3% in 2QFY25/26 (4Q25), according to Minister of Planning and Economic Development, Ahmed Rostom. The Minister projected that the annual growth rate would reach 5.2% by the end of the current fiscal year, exceeding the announced plan targets by 0.7pp. At the sector level, the Minister clarified that the Suez Canal recorded a 24.2% increase, followed by restaurants and hotels at 14.6%, non-petroleum industries at 9.6%, and wholesale and retail trade at 7.1%. The transport and storage sector also saw growth of 6.4%, electricity 5.6%, health 4.6% and education 3.3%. Non-petroleum manufacturing was the largest contributor to the increase, accounting for 1.2pp of the headline growth number.

The Future of Egypt Fund is ready to list its companies on the stock exchange. The fund seeks to implement acquisitions, strengthen the operational capacity of the acquired assets and boost their capital. Once any company has been operating for more than three years, the fund will proceed with its listing on the stock exchange.

The IMF on Wednesday said it completed two reviews of Egypt's economic reform programme, as well as another review under the Resilience and Sustainability Facility (RSF) programme, allowing the country to draw USD2.27bn.

Macro releases (January stats):

- Inflation was 11.7% y/y (Dec: 12.3%).

- FX reserves were USD 52.6bn (Dec: USD 51.59bn).

- PMI decreased to 49.8 (Dec: 50.22).

KENYA

East African Breweries has reported a sharp improvement in interim earnings for the six months to December 2025, with profit rising 38% and revenue reaching a record KSh 76bn, as stronger volumes, margin recovery, and lower leverage offset weak consumer spending and rising illicit alcohol penetration across the region.

President William Ruto has held discussions with the International Finance Corporation (IFC) as Kenya advances plans to establish a National Infrastructure Fund (NIF), as the proposed fund's founding bill moves through the legislative process.

Macro releases (January stats):

- Inflation was 4.46% y/y (Dec: 4.5%).

- PMI slide to 51.9 (Dec: 53.7).

- 2q23 current account deficit widened to KES 138.7bn (USD 920m).

- The Central Bank of Kenya (CBK) anticipates GDP growth for 2023 at 5.7%.

MOROCCO

LabelVie, Morocco’s largest formal retailer, recorded a 12.9% increase in consolidated turnover to MAD 18.5bn due to (i) a 3.5% growth in like-for-like sales, driven in particular by a favorable macroeconomic environment and an improvement in footfall, and (ii) a positive scope effect in connection with the opening of 141 new points of sale as compared to 91 in 2024.

Macro releases included (January stats):

- Inflation was -0.8% y/y (Dec: -0.3%).

- Gross investments into Morocco slowed, down -3.1% in 2q23 (2q22: -8.4%).

MAURITIUS

Macro releases (January stats):

- Inflation was 3.9% y/y (Dec: 4.5%).

- Bank of Mauritius (BoM) moved the interest rate to 4.5%.

COMPANY UPDATES

Key to brackets: (country, industry)

MARKET OUTLOOK

Africa is expected to outperform the rest of the world with an improved outlook in 2026. We continue to allocate to high quality businesses; those that score highly on our internally developed, Likert Q-scoring system, both currently and over time. We have two additional quantitative overlays, valuation and growth. We also have two qualitative overlays being management and ESG. What is particularly exciting is that we have a number of businesses across Africa that fit these criteria. The key transformational trends of financial inclusion, urbanisation and economic formalisation underpin a robust African consumer story that is taking shape regardless of global volatility. We allocate to the best companies in the sectors that tap into this transformation. At the moment, we have a bias towards financial inclusion and fintech themes as they do particularly well on our growth metrics.

Nigeria – The new President is taking reforms seriously, a hugely positive signal to the markets. The communications, fintech and banking sectors are growing strongly, yet high quality companies exploiting these, are at all time low valuation multiples.

Egypt – The short term outlook for Egypt is extremely positive on the back of the UAE real estate deal, the IMF and the World Bank deals. The tourism outlook has improved, wheat prices have halved, and strong remittance growth has returned. With the bulk of household consumption in cash, the investment opportunity for us in fintech is immense in this 100m population country and it will also drive economic formalisation and increased government revenue through widening of the tax net.

Morocco – Morocco’s key economic drivers are mining, agriculture and tourism. Tourism is rebounding with positive indicators for 2026. In terms of outlook, it remains a stable, mid-growth country with excellent opportunities in retail, manufacturing and fintech.

Mauritius – Tourism rebounded and growth prospects are positive.

Kenya – Continued recovery in tourism, lower soft commodity import prices and a rebound in food exports should provide tailwinds. Corporate expansion into neighbouring countries such as the DRC and Ethiopia, provide significant opportunities for Kenya. Safaricom and Equity Group are the two main drivers. IMF and World Bank support will also allow the country to maintain a strong growth trajectory.